Adjustable Bed Insurance Eligibility Estimator

Adjustable Bed Coverage Estimator

Check your potential eligibility for insurance reimbursement

Waking up with back pain or struggling to breathe at night is miserable. If you are in this boat, you might have heard that a doctor can prescribe an adjustable bed is a motorized sleeping surface that allows users to elevate the head and foot sections independently. Also known as electric hospital beds, these devices are often touted as essential for chronic pain management. The big question isn't just whether they help-it's whether your insurance will pay for them. Many people assume that if a doctor writes it down, the insurance company must cover it. Unfortunately, the reality is far more complicated.

The Short Answer: It Depends on the Definition

Technically, yes, a doctor can write a prescription for an adjustable bed. However, a prescription does not automatically mean financial coverage. In most healthcare systems, including those in Australia and the United States, standard adjustable beds sold by furniture retailers are considered consumer goods, not medical devices. Insurance companies typically classify these as luxury items unless specific medical criteria are met.

To get coverage, the device usually needs to be classified as Durable Medical Equipment (DME). This distinction is crucial. A fancy leather adjustable base from a high-end bedding store will almost never be covered. A basic, medically necessary electric bed frame prescribed for a specific condition might be, but the path to approval is steep.

When Is an Adjustable Bed Considered Medically Necessary?

Insurance providers require proof of medical necessity. This means your condition must be severe enough that a standard flat mattress cannot provide adequate relief or safety. Here are the most common conditions that might qualify:

- Sleep Apnea: Elevating the head can reduce airway obstruction. While CPAP machines are standard treatment, some insurers may approve an adjustable bed as an adjunct therapy if CPAP alone is insufficient.

- Gastroesophageal Reflux Disease (GERD): Chronic acid reflux can be managed by keeping the upper body elevated. If medication fails, a doctor might prescribe elevation to prevent esophageal damage.

- Congestive Heart Failure: Patients who struggle to breathe when lying flat may need their heads elevated to maintain oxygen levels during sleep.

- Severe Back Pain or Sciatica: If physical therapy and medication fail, elevating the knees or hips to relieve spinal pressure might be deemed necessary.

- Edema (Swelling): Elevating the legs above heart level can help reduce fluid buildup in patients with poor circulation.

Note that "general comfort" or "better sleep quality" is rarely accepted as medical necessity. The documentation must link the bed directly to treating a diagnosed pathology.

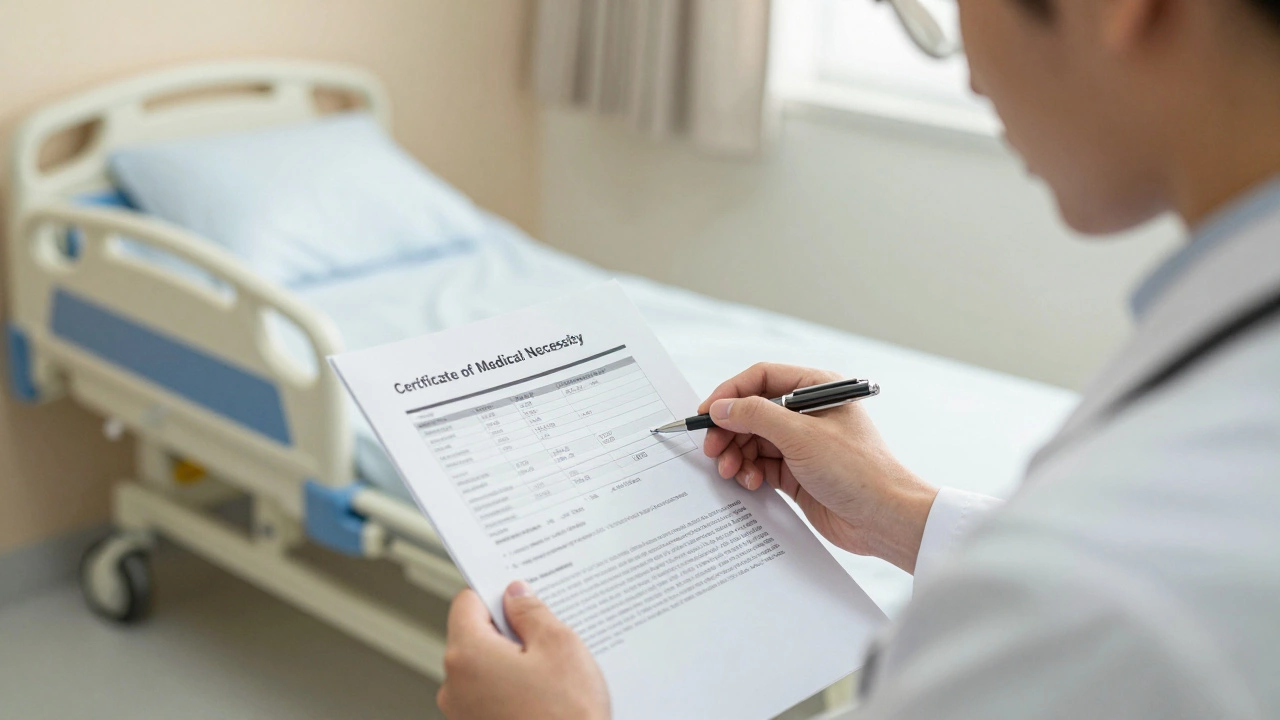

The Role of the Doctor: More Than Just a Signature

Your doctor plays the pivotal role in this process. They don't just hand you a slip of paper. They must complete a detailed Certificate of Medical Necessity (CMN) or equivalent form required by your insurer. This document requires specific data points:

- Diagnosis Codes: Specific ICD-10 codes that justify the equipment.

- Treatment History: Proof that conservative treatments (medication, physical therapy, standard mattresses) have failed.

- Functional Limitations: A description of how the patient’s condition limits their ability to care for themselves or sleep safely without the device.

- Duration of Need: Whether the need is temporary (post-surgery) or permanent (chronic disease).

If your primary care physician is hesitant, consider seeing a specialist. Sleep specialists, pulmonologists, or orthopedists are often more familiar with the documentation requirements for DME than general practitioners.

Insurance Coverage: What Actually Gets Paid For?

This is where most applicants hit a wall. Even with a perfect prescription, coverage varies wildly.

| Provider Type | Typical Coverage | Common Exclusions |

|---|---|---|

| Medicare (US) | Rarely covers full adjustable beds; may cover basic hospital-style frames under strict DME rules. | Luxury bases, memory foam mattresses, wireless remotes, USB ports. |

In Australia, private health insurance generally excludes adjustable beds under hospital or extras cover, viewing them as home furnishings. Some limited assistance might come through government schemes like the National Disability Insurance Scheme (NDIS) if the bed is part of a broader disability support plan, but this is case-by-case and requires extensive assessment.

Private US insurers often follow Medicare guidelines. They might cover the *mechanism* (the motors and frame) but not the *mattress*. You would likely still have to buy the mattress out-of-pocket.

Alternatives to Full Coverage: How to Lower the Cost

If your insurance denies the claim, you aren't completely out of luck. There are strategies to make an adjustable bed more affordable:

- FSA/HSA Accounts: In the US, Flexible Spending Accounts and Health Savings Accounts allow you to use pre-tax dollars for eligible medical expenses. An adjustable bed is often eligible if accompanied by a Letter of Medical Necessity from your doctor.

- Medical Financing: Companies like CareCredit offer financing plans specifically for medical equipment, sometimes with interest-free periods.

- Manufacturer Rebates: Some brands partner with medical suppliers to offer discounts for patients with documented conditions.

- Used Medical Equipment: Local DME suppliers often sell refurbished hospital-grade beds at a fraction of the retail price. These lack the aesthetics of bedroom furniture but perform the same function.

The Mattress Factor: Don't Forget the Top Layer

An adjustable bed frame is useless without a compatible mattress. Standard innerspring mattresses often crack or break when bent repeatedly. You need a flexible material.

Memory foam is a viscoelastic polyurethane foam that conforms to the body's shape and remains flexible when articulated. This is the gold standard for adjustable bases. Latex is another good option because of its natural elasticity. Avoid rigid hybrids or traditional coil springs unless they are specifically marketed as "flexible" or "articulating."

Interestingly, while the frame might be partially covered, the mattress is almost always excluded. When budgeting, factor in that you will likely need to purchase a new, flexible mattress alongside the base.

Steps to Get Your Prescription Approved

If you believe you qualify, follow this checklist to maximize your chances:

- Consult Your Specialist: Discuss your symptoms and explicitly ask if an adjustable bed could help. Mention that you are seeking DME coverage.

- Request a Detailed Letter: Ask for a Letter of Medical Necessity (LMN). Ensure it includes your diagnosis, why other treatments failed, and why the specific features of the bed are needed.

- Contact Your Insurer First: Call the member services number on your card. Ask exactly what documentation they require. Do not assume the doctor knows their specific forms.

- Submit via a DME Supplier: Often, you cannot buy the bed directly from a retailer like Amazon or Wayfair and seek reimbursement. You must purchase through a certified DME supplier who handles the billing and prior authorization paperwork.

- Appeal if Denied: Initial denials are common. If denied, request a peer-to-peer review where your doctor speaks directly to the insurance medical director.

Conclusion: Weighing the Investment

While a doctor can certainly prescribe an adjustable bed, securing full payment from insurance is difficult and often unrealistic. For many, the investment pays off in improved sleep quality, reduced pain medication reliance, and better overall health. If coverage falls through, exploring FSA/HSA options or financing can bridge the gap. Always prioritize the medical mechanism over luxury features if cost is a concern.

Will Medicare pay for an adjustable bed?

Medicare rarely pays for adjustable beds. They may cover a basic, non-luxurious electric hospital bed if it is deemed medically necessary for a condition like severe arthritis or mobility issues, but it must be purchased through a Medicare-approved DME supplier. Luxury features and mattresses are never covered.

Can I use my HSA or FSA to buy an adjustable bed?

Yes, in many cases. If your doctor provides a Letter of Medical Necessity stating the bed is required to treat a specific medical condition, you can typically use funds from a Health Savings Account (HSA) or Flexible Spending Account (FSA) to purchase it.

What is the difference between an adjustable bed and a hospital bed?

A hospital bed is designed for clinical care, featuring side rails, higher weight capacities, and simpler mechanisms. An adjustable bed is designed for home use, focusing on aesthetics, quiet motors, and comfort features like zero-gravity positioning. Insurance is more likely to cover a hospital-style bed than a luxury adjustable base.

Do I need a special mattress for an adjustable bed?

Yes. Traditional innerspring mattresses can break when bent. You should use a memory foam, latex, or specifically designed flexible hybrid mattress. Using a non-flexible mattress on an adjustable base may void the warranty and damage the mattress.

How do I appeal an insurance denial for an adjustable bed?

First, request a detailed explanation of the denial. Then, ask your doctor to submit additional documentation or request a peer-to-peer review with the insurance company's medical director. Provide any additional studies or letters that support the medical necessity of the device for your specific condition.